Budgeting Tips for Beginners

According to a recent study, 78% of Americans are living paycheck to paycheck.

Um, what?! That number is crazy high!! I don’t know about you, but I think that number needs to come down, like a lot.

The thing is, in order to stop living paycheck to paycheck, you need a plan for how to work with your money (and how to STOP working against your money and your goals).

And, you guessed it, that plan is also known as a BUDGET.

Does the word budget scare you? Make you want to run and hide? Feel like the worst chore on your to do list?

I promise, it isn’t that bad or that scary. It is simply a plan for your money. That is it.

See, that isn’t so bad. So if budget is the new B-word in your house, you can refer to it as The Money Plan. Easy. Done.

Creating a Budget (or Money Plan) is the only way to get in control of your finances and realize your dreams.

Sticking to our budget is how we were able to payoff my husband’s dental school loans (over $300k of them!) in less than 3 years. It can be done!

So, how do you create your own Money Plan? The steps are actually pretty simple and I will walk you through them in this beginner’s guide to budgeting.

Need to come back and read this later? Make sure to pin it where you can find it!

4 Steps to Preparing a Budget

1. Know your Income

In order to start your budget and know how to manage your money, you have to know how much you actually have to work with.

For some people, this is a no brainer–they get a steady, salaried paycheck that comes regularly during the month, or every two weeks, and it is always the same amount.

If that is you–congratulations. Look at your paystubs for last month. Add your take home pay together and voila! You now know your income.

For others, this step may be harder–hourly jobs that change hours, self-employed jobs where income isn’t predictable, etc.

If you are in this category your task here may be a little more difficult. So what I want you to do is look at your income for the last three months, add up how much you brought in from the different sources in each of those months.

Then take the smallest amount from those three months and use that as your baseline income–the income we will work with.

Anything you get in future months above and beyond that number will be bonus.

If you receive a lot of cash as income, and haven’t been good about tracking how much comes in, I want you to start tracking it right now.

You need to know how much you have coming in.

And remember, learning to budget and managing money is meant for now and the long term.

So it is okay to track income for a few weeks or a month to see where you stand. You need accurate numbers to make an accurate plan.

2. List Your Expenses

Okay, here is where you can get a little caught up. Some items you spend money on you should know right away–they are the same every month (things like Rent, car insurance, etc.)

But with other expenses, the monthly amount will change from month to month. So there are 2 good ways to tackle this piece.

1. Track Expenses from your bank account. Take a look at your bank account and credit card transactions for the last 3 months. Give every item an expense name (groceries, utilities, fun, eating out, etc.) Then add up all the items in each category, for each month. This will help you see how much you have spent in the past on each category. And seeing how much you spent will let you know what to plan for in the coming months.

2. Start Tracking Expenses Now. Option two is to start tracking every dollar that you spend, starting right now. Track what you spend your money on for 30 days. After the 30 days, see how much you have spent in each category.

RELATED ARTICLES

7 Budget Categories for a Simple Budget

A Sample Budget to Help you Create a Budget

8 Tips to Help you Stick to a Budget

3. Make Your Plan

Now comes the part where you actually make your Money Plan (aka budget). Once you have your income and you know how much you spend (and on what) throughout a month, you can start to make conscious choices on where you money should go.

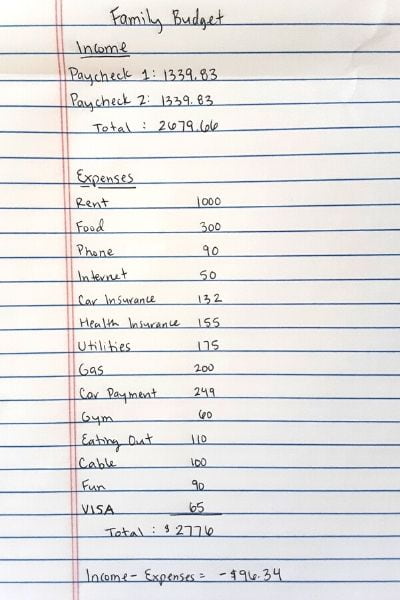

Grab a good old piece of paper.

Work with me on this. Writing a budget all down on a piece of paper really helps to drive home the need to make a budget work.

When you see it all in black and white, it is much harder to ignore. You can do a template on the computer later on (I have a budget template that I love), but for now stick to pen and paper.

At the top, write what your baseline monthly income is. Then, below that, list all your expense categories and how much you are spending on each item.

Next see how your income compares to your expenses. Take your income and subtract your expenses from the income amount. Your paper might look something like this:

Does the result scare you? Make you feel relieved? Anxious? Incredulous? All emotions are completely fine. This is why we write it down–to see it and see where we can make changes for the better.

If your expenses are more than your income, it is time to start going through them and see where you can cut some expenses to free up some more money.

What non-essentials could you do without for awhile? Could you do without cable? Eat out less often and eat at home to save on food? Or could you go more drastic and sell that car and get a cheaper one?

RELATED ARTICLE: HOW TO BUDGET WHEN MONEY IS TIGHT

Again, getting your money under control is a process and sometimes we need to sacrifice, just for a little while, in order to reach our goals. It won’t be forever, but it will be worth it.

The goal is to get your expenses down so that income-expenses=$0. This is called a Zero Based Budget. And it is the process of giving every dollar that comes into your bank account a job to do.

So now that you have paired down your expenses, it is time to rework your paper so that your expenses match the new numbers you have figured out.

Decide how much you plan to spend in each expense category and write it down (hint–debt payments and saving for various items also count as expense categories).

This is your new Money Plan and what you will work off of moving forward. Your paper should look something like this now:

Congratulations! You have made your personal money plan! Now you need to use it.

4. Do It Again and Again

A budget is only good if you use it and revisit it consistently. Plan to check in with your budget every 2 weeks to 1 month.

Don’t worry if you went over budget on something. Figure out what happened, how you could do better and plan to move forward.

The biggest thing is to not give up! No one is perfect, and your first budget won’t be perfect either. But keep working it, revising it and eventually you will have a plan that works for you and your household.

If you do, you will be on your way to achieving your financial goals, getting out of the paycheck to paycheck hamster wheel and moving toward true financial freedom.

Let me know if I can help. And leave a comment letting me know if you have any questions!

RELATED ARTICLES:

How to Live on $2500 per month

Bare Bones Budget

11 Sinking Funds Your Budget Needs

Beginner’s Guide to Budgeting in 4 Easy Steps

Want to save this article for later? Make sure to pin it to Pinterest!